Intel Q2 FY 2019 Earnings Report: Datacenter Drop

by Brett Howse on July 26, 2019 12:15 AM EST- Posted in

- CPUs

- Intel

- Financial Results

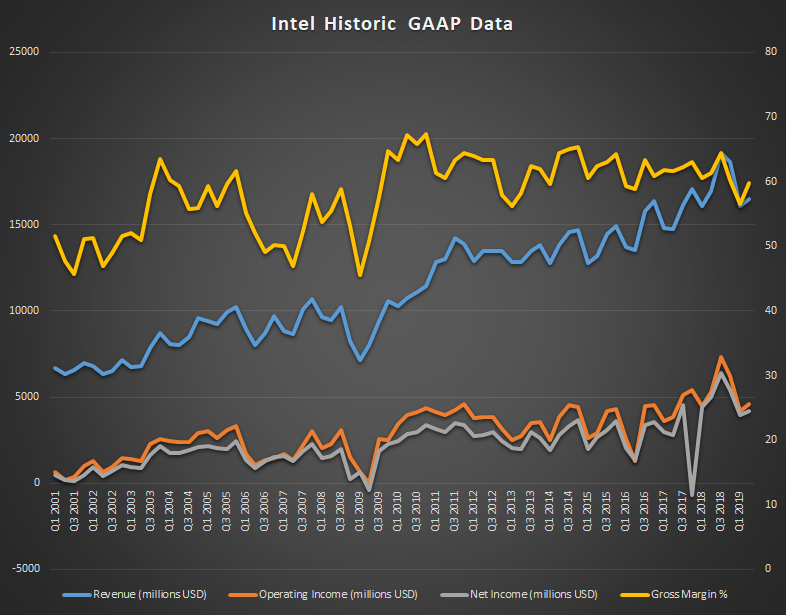

Intel announced their earnings for the second quarter of their 2019 fiscal year. Overall, revenue dropped 3% year-over-year to $16.5 billion, with gross margins still below the 60% that Intel likes to maintain, but at 59.8%, the are improved significantly over last quarter’s 56.6%. Operating income for the quarter was down 12% to $4.6 billion, and net income down 17% to $4.2 billion. This resulted in earnings-per-share of $0.92, down 12% from a year ago.

| Intel Q2 2019 Financial Results (GAAP) | |||||

| Q2'2019 | Q1'2019 | Q2'2018 | |||

| Revenue | $16.5B | $16.1B | $17.0B | ||

| Operating Income | $4.6B | $4.2B | $5.3B | ||

| Net Income | $4.2B | $4.0B | $5.0B | ||

| Gross Margin | 59.8% | 56.6% | 60.6% | ||

| Client Computing Group Revenue | $8.8B | +2% | +1% | ||

| Data Center Group Revenue | $5.0B | +2% | -10% | ||

| Internet of Things Revenue | $986M | +8% | +12% | ||

| Mobileye Revenue | $201M | -4% | +16% | ||

| Non-Volatile Memory Solutions Group | $940M | +3% | -13% | ||

| Programmable Solutions Group | $489M | +1% | -5% | ||

Over the last couple of years, it’s been the datacenter group that has been the sharp end of Intel’s growth, and it’s now the datacenter group that took the brunt of the slowdown. In fact, the PC-centric group at Intel managed to keep revenue more or less flat compared to last year, up 1% from Q2 2018, with $8.8 billion in revenue. Intel has seen high sales in their higher performance, and therefore higher margin, products, as well as customers purchasing ahead of possible tariffs. Intel also has finally started shipping 10 nm products in volume with expectations of holiday 2019 sales. The Client Computing Group had operating income of $3.7 billion this quarter, up from $3.2 billion a year ago, so despite Intel not executing on 10 nm as expected, they are still quite strong in the PC space even as competition has ramped up.

Intel’s Datacenter group experienced a revenue drop of 10%, with $5.0 billion in revenue for Q2. The biggest single drop was enterprise and government revenue, which was down 31%, but cloud also declined, although only 1% compared to last year, and the communications service provider segment was up 3%, offsetting some of the drops. Operating income for the Datacenter group was down more significantly though. Operating income was $1.8 billion, down 34% from a year ago.

Intel’s Internet of Things continues its rise, almost hitting the $1 billion/quarter threshold, and achieved a record quarterly revenue for Q2 with $986 million in revenue. This was up 12% from a year ago, with increased demand for higher performance processors driving the revenue gain. Operating income was up $51 million to $294 million as well. Mobileye revenue was up 16% to $201 million with an operating income of $53 million, up 20.4%.

Intel’s NAND group had revenue of $940 million in the quarter, down 13% due to “challenging pricing” and Intel continues to lose money on their NAND group, with an operating loss of $284 million this quarter, compared to a $65 million loss last year.

Finally, Programable solutions had revenue of $489 million, down 5% from last year with no explanation given. This group saw its operating income slashed almost in half compared to last year, coming in at $52 million for the quarter compared to $101 million a year ago.

Collectively, Intel’s PC group was up 1% and its Datacenter products were down 7%. Intel saw a 2% drop in notebook processor volumes, but average selling price was up 3%. Desktop processor volumes were down 11% compared to Q2 2018, but average selling price was up 5%. On the datacenter side, unit volumes were down 12% compared to Q2 2018, and average selling price was only up 2%.

Looking ahead to Q3, Intel is expecting revenues of around $18.0 billion, with earnings-per-share of about $1.16.

Source: Intel Investor Relations

16 Comments

View All Comments

CityBlue - Friday, July 26, 2019 - link

We're still waiting for the Anandtech "deep-dive" on Intel vulnerabilities and resulting performance losses. Are Intel still fobbing you off as you claimed? I guess the article isn't really going to appear after all, is it guys? Your credibility is approaching zero... only Intel fluff pieces from Anandtech in future, look elsewhere for critical and unbiased analysis.wilsonkf - Friday, July 26, 2019 - link

Wasting time doing a "deep-dive" now - make no sense if new flaws are coming out every six or seven months.CityBlue - Friday, July 26, 2019 - link

You're right it's a waste of time 6 months or whatever later, but that doesn't mean we should forget that Anandtech chose to look the other way (while fobbing off enquiring readers saying they were waiting on answers from Intel) rather than being critical of Intel. And this is going to be repeated in future, hence the lack of credibility they now have. Anandtech are quick to write fluff pieces that show Intel in a positive light, but anything critical (regardless of it's importance) we know will be non-existent. It's hard to take Anandtech seriously under such circumstances, particularly when other sites are discussing the issues that Anandtech ignores.ballsystemlord - Friday, July 26, 2019 - link

I too have been waiting patiently for their analysis and worry, as you do, that it will never come; at least until Intel releases a set of products with all of the vulnerabilities, fixed and then Intel will say, "See how much faster our new parts are!" and AT will confirm it.I dislike being so cynical, but what choice do I have?

Carmen00 - Friday, July 26, 2019 - link

Relax, cowboy. If everyone else is writing these pieces, go read 'em elsewhere. I'm happy to wait for Anandtech to do their painstaking and detailed in-depth pieces properly ... and if you're not, that's your choice, fine. Though how you call THIS article on earnings a "fluff piece" is beyond me!PeachNCream - Friday, July 26, 2019 - link

Yeah, like the detailed in-depth performance analysis of Rivet Networks' Killer NIC series of products that clearly demonstrates how they were worth all of the off-handed remarks about how good they would be for the buyers. Or that coverage of the GTX 1050, and the 1030, the MX150, and a bunch of AMD graphics cards from the last couple generations. Those were all well-developed, well-written articles free from copy-paste table errors and embedded auto playing advertising videos.Carmen00 - Friday, July 26, 2019 - link

I see your point. On the other hand, there are a mere handful of sites that I trust as much with journalistic integrity and in-depth knowledge as Anandtech. They've carried on in much the same way as they have when Anand Lal Shimpi was leading them ... with a few more ads, perhaps, but that's a minor enough issue for me (and no, I don't use an ad-blocker, they deserve the revenue). They're certainly not perfect and I don't claim that they always get everything completely correct; who does? But I DO claim that they are not overtly biased and they try not to be biased, which is what the original poster has his underpants in a knot about.If you know of other (or better) sites to recommend that cover the area with a similar mix of breadth, depth, and journalistic integrity, I'd like to know what they are. Really, I would... without as much time as I'd like these days, I find myself seeking high-quality material. Anything else (and especially the clickbait pit that journalism has descended into) is a waste.

PeachNCream - Friday, July 26, 2019 - link

The silence should not surprise you.HStewart - Friday, July 26, 2019 - link

Please research like this belongs on WCCFTech, AnandTech should spend time on more critical issues. No body has yet shown a single real virus from any of this spectrum/Meltdown BS and keep in mind it not just Intel that is related to issues. AMD and ARM cpus have been proven to also have variants.Qasar - Friday, July 26, 2019 - link

sorry HStewart, but most of the issues you are referring to ONLY effect intel's chips, but please, feel free to post a link that shows other wise...yet again, as usual, here's HStewart, trying to make bad news towards intel, look like good news, or look positive, when its negative